Not long ago, those who had health and dental insurance benefits through their workplace could look forward to continuing those benefits in retirement. However, that’s often not the case anymore.

Every working Canadian needs to learn more about the future of health insurance for retirees in Canada.

The Current State of Health Insurance in Canada

Currently, many working Canadians are covered by the health and dental insurance benefits that are provided through their place of employment. This coverage often extends to their spouse and eligible dependents. Because this coverage comes as part of the overall workplace compensation, it can be taken for granted. Consumers often have no idea how much these benefits cost, whether or not the coverage is adequate for their needs, or if those benefits can follow them into retirement.

These private health and dental insurance plans provide some measure of cost protection against healthcare expenses that are not covered by provincial health insurance, like medical equipment, physiotherapy, prescription drugs, and private or semi-private hospital rooms. Dental insurance is also commonly included in these employer-provided plans.

Many of those who do not have workplace benefits are already aware of the high costs associated with paying for these services out of pocket. Those who have not factored the costs of healthcare in retirement into their budget, or assume that their workplace will continue to provide assistance, are in for a big surprise.

Health Insurance in Canada: The Next 20 Years

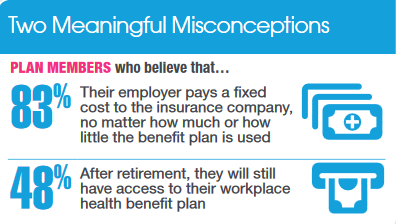

Every year, Sanofi Canada conducts a survey of employers about their future plans for health care. The Sanofi Canada Healthcare Survey is widely considered to be a leading source of information on the present and future state of health insurance in Canada. The 2015 report is eye-opening for many reasons, not the least of which is the forecast for the future of health insurance for retirees.

According to the report (pp. 31–32), many employees are unsure about what will become of their employer-sponsored benefits upon retirement:

“Twenty-six percent of plan members do not know what will happen to their health benefit plans when they retire, a finding that is consistent across breakdowns for size, labour environment and public versus private sectors… Among remaining employees, 25% expect their current workplace benefit plan to continue—jumping to 40% among employees closest to the age of retirement.”

There is a substantial difference between employee perceptions about benefits, and what employers have to say about the availability of benefits in retirement:

“Thirty-five percent of plan sponsors, meanwhile, indicate health benefit plans are available after retirement—but only 6% do so at no cost to the retired plan member.”

The Disturbing Misconception That Health Benefits Continue in Retirement

Almost five years after that report, Canadian workers are still unclear about who will pay for healthcare during their retirement years.

The Sanofi 2019 survey discovered the disturbing fact that 48% of retiring plan members believed they will have access to workplace health benefits – and that simply is not the case.

Clearly, there is room for improvement in the communications around health and dental insurance for retirees in many workplaces. However, the onus falls on those future retirees to ensure their health and dental insurance needs are covered when they leave the workplace.

Retirees Must Budget for Major Health Events

Nobody likes to think about the worst-case scenario, which is why so many of us do not plan for a major health crisis in retirement. It makes the numbers on the financial planning chart look sound, but it’s not a realistic long-term strategy.

Consider this: Nearly six of 10 older Canadians say they have experienced a “major life event” that disrupted the financial plans they had in place according to the Ontario Securities Commission report on the financial stages of older Canadians. From unexpected early retirement to a serious health crisis that put a drain on family finances, many things that are out of our control can affect retirement plans.

In light of this, it makes sense to do everything in our power to guard against preventable expenses that can be a serious drain on a fixed income.

Make Sure You Have Private Health Insurance to Bridge the Gap

The best way to help safeguard against the financial hardship of paying for medical expenses and treatments out of pocket in retirement is to have your own personal health insurance plan in place. Plans are available to retirees who are just coming off a group benefits plan, where you can take advantage of guaranteed coverage if your application is completed within 90 days of losing your group benefits.

Working with an SBIS insurance expert can help you identify the plan that best suits your needs and your budget. Contact us today to get started on the right health insurance package to help protect your financial future.

{kind=link}

My group plan benefits expire on Sept 30, 2020.

Hi Wendy,

We’d be happy to help you get a health insurance plan to cover you after your group plan expires.

To get a health insurance quote, you can fill out the questionnaire at the top of our health insurance page: https://sbis.ca/health-insurance.html

Alternatively, you can call us to speak with a live agent at 1-800-667-0429, Monday to Friday, between 8:45AM to 4:45PM EST.